The role of a professional footballer has changed drastically over the decades. Earlier, a player was just another employee at a club – rendering his services and drawing his wages. But now, with top teams becoming multi-national corporations with a presence that spans the entire globe and so many streams of revenue opening up for them, the players are no longer just regular staff members or HR personnel.

A club these days earns its revenue from three primary sources. First is the matchday revenue that includes sale of tickets on matchdays and membership fees. Second is the broadcasting revenue, received by the club for its matches being broadcasted on TV all across the world. Lastly, we have the commercial revenue that the team receives from sponsors and through the use of its intellectual property rights i.e. merchandise bearing the team name and logo.

Another question that can be asked is – what is the real source of all this income? In the end, it all boils down to the players who take to the pitch every week and it is with their performances, that the team earns all that cash from all over the world. With the global reach of football clubs these days and devoted fan bases in all continents, the players no longer remain just employees. They are their clubs' strategic assets – both tangible as well as intangible in a way.

The world-record fee that Real Madrid splashed out for Cristiano Ronaldo in 2009 was not just for his footballing ability. The jerseys bearing his name that are sold all over the world help the Los Blancos rake in millions every fiscal year. Another example would be the signings of Park Ji-Sung and Shinji Kagawa by Manchester United, who apart from their contributions on the Old Trafford pitch, also filled the club’s coffers by engaging millions of fans in South Korea, Japan and even beyond.

In financial accounting terms, an asset is an economic resource. Anything tangible or intangible that can be owned or controlled to produce value and that is held to have positive economic value is considered an asset. Simply stated, assets represent value of ownership that can be converted into cash.

Players are more than just employees at a football club

Considering all the evidence from the above paragraphs, it is safe to conclude that the players we watch, follow and read about every day are more than just employees of their clubs. They are like any other capital asset - be it land, machinery, building or goodwill. Lionel Messi and Neymar are as much revenue-generating assets for FC Barcelona as the Camp Nou itself, if not more!

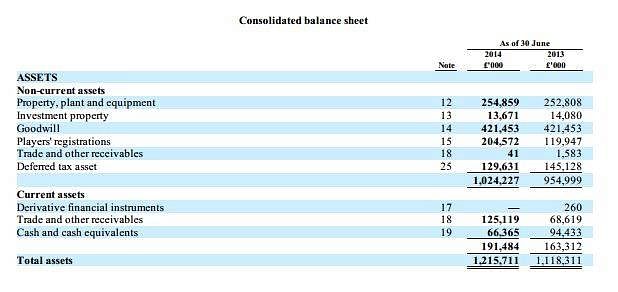

Further evidence regarding this statement can be extracted from the financial statements of the clubs themselves. An analysis of the 706-page long Annual Report from 2014 submitted by Manchester United PLC (Public Limited Company) to the New York Stock Exchange provides a clear picture as to how players are treated in accounting terms and how they are shown as assets in the balance sheet.

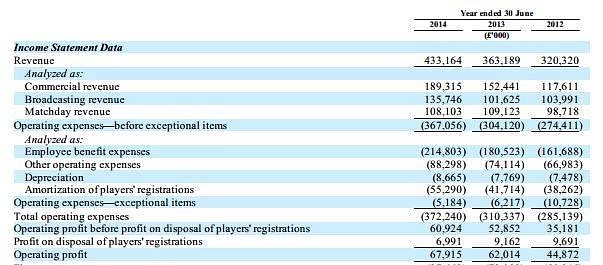

From the document, it can be inferred that the accounting treatment for player registrations are in no way different from any other capital asset. The cost of acquisition of a player is amortized over the period of his contract using the simple straight-line method. If a player extends his contract prior to the end of the pre-existing period of employment, the remaining unamortized portion of the acquisition cost is amortized over the period of the new contract. The amount amortized each year is displayed in the Income and Expenditure Statement as an expense and like the depreciation charged on any other asset, it reduces the operating profit for the financial year.

Page 62 of the Annual Report reads - “The Amortization of players' registrations for the year ended 30 June 2014 was £55.3 million, an increase of £13.6 million, or 32.6%, over the year ended 30 June 2013. Increases in amortization due to player acquisitions during the year (mainly Fellaini and Mata) were partially offset by reductions due to departed players (mainly Berbatov). The unamortized balance of existing players' registrations as of 30 June 2014 was £204.6 million, of which £66.9 million is expected to be amortized in the year ended 30 June 2015. The remaining balance is expected to be amortized over the three years ending 30 June 2018.”

What about the wages of the players then? Well, they can be seen as operating expenses with respect to the assets that are the players themselves. Like repairs and maintenance for plant and machinery, the weekly compensation received by the players can be treated as recurring expenses which also reduce the profit for the accounting period. The basic weekly wage along with multiple contractual bonuses, benefits and insurance contributions that the players are entitled to as well as their training costs are nothing but those incurred for the proper working of the asset – that is the player himself.

All in all, one can easily say that professional footballers at the top level of the game are income-generating assets for their clubs, who are now billion-dollar organizations with a reach that encircles the entire planet. A glance at a team’s accounts seems to suggest the same.