'%20x='0'%20y='0'%20height='100%25'%20width='100%25'%20%0A%20%20%20%20%20%20%20%20%20%20xlink%3Ahref='data:image/jpg;base64,/9j/2wBDAAYEBQYFBAYGBQYHBwYIChAKCgkJChQODwwQFxQYGBcUFhYaHSUfGhsjHBYWICwgIyYnKSopGR8tMC0oMCUoKSj/2wBDAQcHBwoIChMKChMoGhYaKCgoKCgoKCgoKCgoKCgoKCgoKCgoKCgoKCgoKCgoKCgoKCgoKCgoKCgoKCgoKCgoKCj/wgARCAAGAAoDASIAAhEBAxEB/8QAFQABAQAAAAAAAAAAAAAAAAAAAgf/2gAIAQEAAAAAED//xAAUAQEAAAAAAAAAAAAAAAAAAAAD/9oACAECEAAAAB//xAAUAQEAAAAAAAAAAAAAAAAAAAAD/9oACAEDEAAAAF//xAAgEAACAgEDBQAAAAAAAAAAAAACAwEEBQAGEQcUISJy/9oACAEBAAE/AKmbxeL6V41zKpQ0gRWNk11v94KBOeJkfBfWtz36NvcuWsUe5r1HW3MSmFgMLCTmRHiNf//EABgRAAIDAAAAAAAAAAAAAAAAAAECAAMR/9oACAECAQE/AKmLaTP/xAAYEQACAwAAAAAAAAAAAAAAAAABAgADEf/aAAgBAwEBPwC1QoGT/9k='%3E%3C/image%3E%3C/svg%3E)

There is a popular saying that it is very easy to take £1 million out of a football club. All you have to do is first invest £2 million. The general sentiment of that statement is not far from the truth. Most football club owners are not in it to make money, even though modern football is a business; of that there is no doubt. The cultural and sentimental aspects of the sport however, ensure that football clubs operate on different economic (and often legal) rules from most businesses.

The existing transfer system places restraints on workers in ways that would be held illegal by European courts if it was applied to just about any other industry. The famous Bosman and Webster cases that gave players more power to decide where they would ply their trade (although the ruling in the Matuzalem case that more or less overruled the Webster ruling swung the pendulum back in favour of the clubs) were borne out of an attempt to harmonize European law with the existing football system.

Football clubs are usually not sound investments. It can be years, or even decades before any investor begins to see anything resembling a decent return on the investment. Roman Abramovich has already invested close to £1 billion pounds in Chelsea, with that figure set to rise if he does indeed go ahead with the construction of the proposed new stadium. Sheikh Mansour at Manchester City is in a similar situation. Mike Ashley at Newcastle is in the unique position of having spent more than £200 million on his boyhood club, and being detested by its fans. He too is unlikely to see any of this money returned.

In spite of this, there is a constant line of wealthy investors willing to buy Premier League clubs. Many owners are rich fans who want to facilitate successful performances by their clubs. There are also those people who are not particularly concerned with sentiment or finances, but instead seek to take advantage of the various intangible benefits of owning a club (such as celebrity, public and brand recognition, and access to important people).

How to buy an English football club

Football clubs are separate legal entities in themselves. The organisational structure of clubs however, varies from club to club. Broadly speaking, clubs may be registered as companies (either public or private) or as member-owned non-profit sports organisations (this is commonly referred to as fan ownership).

In a fan ownership model, there is no single owner. Executive decisions are taken by a board of directors that are usually elected by the members of the club (who are the fans themselves), and thus the club cannot be “bought” by any one individual. This type of ownership is not common in England anymore, but Real Madrid and Barcelona are the two most prominent examples of fan-owned clubs (for a more detailed breakdown of Real Madrid’s ownership structure, check this older article).

The German Bundesliga has what is known as the "50 + 1" rule, which mandates that association or club has to have a controlling stake. This is to ensure that commercial interests can't gain control of the functioning of the club. Audi and Adidas each own 9% of Bayern Munich for example, but the rest is controlled by the members via the club.

There are two exceptions to this rule - Wolfsburg are owned by Volkswagen and Bayer Leverkusen are owned by the chemical company, Bayer (this is because both these clubs began as workers’ sporting clubs). However, the rest of the German league follows the “50 + 1” rule.

Public companies

If the club is registered as a public company and listed on the stock exchange, then the standard rules pertaining to takeovers that apply to regular companies would apply to football clubs as well. The most well-known example of a publically listed club is Manchester United. Other famous clubs that are listed on stock exchanges are Juventus and AS Roma.

There was a phase in the late 1990s and early 2000s where English clubs initialized IPOs (Initial Public Offering) of shares in the hopes of raising revenue, but that bubble burst rather quickly. Tottenham Hotspur were publically traded for 10 years from 2001 to 2011, but eventually decided to move back to a private ownership structure.

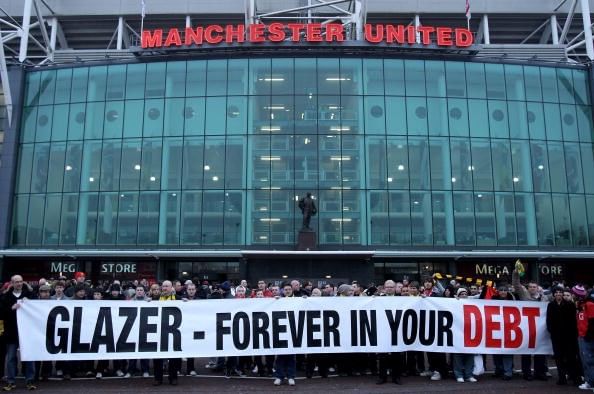

When United were on the verge of being taken over by their current owners (the USA-based Glazer family), it was not as simple a matter of purchasing all the available shares outright. The Glazers initially purchased a 3% stake in the club in March 2003 through their holding company, Red Football. A slow and steady acquisition of shares over the next year brought them to around 15% by November of the same year. It was only then that rumours of a takeover began to emerge.

Takeover law in the UK mandates a compulsory takeover bid by a shareholder when the value of shares held by them reaches 30%. This figure was reached in October 2004, and the bid was subsequently launched. The Glazers continued to acquire shares, acquiring complete ownership of the club by June 2005. A more detailed analysis of the Glazers’ ownership of Manchester United can be accessed in this article.

Private companies

Private companies are not subject to the same regulations that publically listed companies are. For an investor to purchase a private company there has to be an agreement between the existing management and the prospective one for transfer of control of the company for a certain price. In 2007, Liverpool FC were bought by American businessmen Tom Hicks and George Gillett for around £435 million. £185 million was loaned to them by the Royal Bank of Scotland (RBS) to complete the deal.

The takeover also saw guarantees of around £200 million from the two Americans, as well as the financing of the construction of a new stadium for the club. However, the combination of the global economic crisis in 2008-09, as well as Liverpool’s subsequent failure to qualify for the Champions League meant that the club was not in good health financially speaking. The debt and interest payments owed to RBS had reached nearly £237 million, and the club was spending nearly £100,000 per day servicing this debt (To clarify, the debt was held by the holding company, and not the club itself.

This arrangement was similar to the Glazer takeover at Manchester United). A refinancing of the debt agreed with RBS in April 2010 contained a clause saying that the weekly £2.5 million weekly penalties imposed on Hicks' and Gillett's Liverpool holding company would amount to an additional £60m if the club was not sold by 6 October of that year.

Fan protests as well as concern of the board of directors led to a search for new ownership. After a bid from a Chinese consortium fell through, RBS placed the club’s loans in their toxic-assets division; a move that most saw as the end of the Hicks-Gillett reign at Anfield. On the 5th of October, the Liverpool board announced it had received two offers for the club, one of which was from the Fenway Sports Group (the current owners), the American sports conglomerate who owned the Boston Red Sox Major League Baseball team.

Hicks and Gillett deemed the offers to be unacceptable and attempted to oust Christian Purslow and Ian Ayre, Liverpool's managing and commercial directors respectively, from the club's board. However, RBS obtained an injunction from the Royal Courts of Justice preventing the duo from changing the composition of the board, in order to ensure that the sale went through. The sale of the club to FSG was completed the very next day, avoiding the penalty from RBS.

FSG purchased Liverpool for £300 million, and also agreed to repay the loans owed to RBS. The takeover reduced the club’s annual debt servicing costs from £25-30 million to £2-3 million. Hicks and Gillett challenged the sale in courts, both in the US (Texas) and in the UK. The American court granted an injunction against the sale, but the English court ruled that such an injunction was invalid as the matter at hand had nothing to do with Texas. The UK court ruled against Hicks and Gillett, thus validating the sale to FSG. Hicks and Gillett then filed a suit for nearly £1 billion in damages, but the case was settled out of court for (apparently) no sum of money at all.

Ian Ayre later went on to say that the sale to FSG was absolutely critical, as the club was on the verge of being placed in administration at that point. Despite the relative lack of success even after the FSG takeover, the purchase of the club has proved to be a decent investment for the conglomerate as the club was recently valued at £644 million (over 40% increase in value) since it was bought. This is only set to rise with the arrival of the Premier League’s new TV rights deal.

How a club can be sold for £1

In most cases though, the purchase of clubs is far less dramatic. Any prospective owner must agree on a price, as well as agreeing to take on all the liabilities and debts of the club. The agreement regarding liabilities may be either with the creditors directly, or with the existing owners. This principle is what allowed Chelsea’s former owner Ken Bates to buy the club for £1 (yes, one pound!) in 1982. The other part of the purchase was that Bates also had to agree to take on debts of £1.5 million.

Recently, Reading FC were in the news after it was announced that their then-owner Anton Zingarevich was looking to sell the club for just £1. The catch to this was that the new owner would also have to discharge the £38 million in debts owed by the club.

So what is the logic behind asking for just one pound? Under English law, a contract requires the payment of “some consideration” to be valid. The token sum is a symbolic but important part of the contract, showing that "some consideration" has been paid. It could be any sum, as long as it reflects the fact that some sort of payment has been made (For what it’s worth, Reading FC have since been sold to a Thai consortium).

Fit and proper persons

One last thing that any prospective owner of an English club must do is pass the FA’s “fit-and-proper-person test”. This is a test undergone by owners and directors of British football clubs in the hope that it prevents corrupt or untrustworthy businessmen from buying them. For Premier League clubs, the test must be passed before the takeover is completed, whereas the Football League only examines new owners and directors after the takeover has gone through.

The Premier League test disqualifies an owner if he has an interest or influence in another Football League club, if he is filing for bankruptcy, or has been involved in two or more events of insolvency as the director of a football club. This test, however, is mostly a formality, as plenty of unsuitable owners have had no issue passing it.

Examples of these are Thaksin Shinawatra (who was a fugitive from Thailand at the time) buying Manchester City, or Portsmouth passing through the hands of four owners in one season on the way to bankruptcy and relegation. More recent examples include the likes of convicted money-launderer Carson Yeung at Birmingham City, or twice-convicted fraudster Massimo Cellino at Leeds United. Since its introduction in 2004, only four people have failed it.

With the commercial value of football set to rise even further, buying a football club may not be as bad an investment as it was once thought to be. Purchasing a Football League club and securing its promotion to the Premier League can be hugely profitable. Current estimates put the value of promotion from the Championship at £80 million, and this is assuming that the promoted club is relegated instantly after one season.

If they managed to survive just one season in the Premier League, the total revenue for the club from just TV and prize money would be in the range of £180-200 million. Owning an English club now can actually prove to be a good investment if it is handled well, as the new commercial deals and brand recognition of the Premier League have made the purchase of an English club a far less risky investment than it once was.